BlackRock and Coinbase are tokenizing stocks, but the everything app trade is a trap

The market's total volume dropped nearly 20% to $72.46B, which raises questions about whether institutional interest in tokenized assets is actually driving network demand. While the headlines scream about a revolution in finance, the actual pipes are surprisingly quiet. We are seeing a push toward everything apps where your stocks, bonds, and crypto live in one centralized dashboard. On the surface, it looks like efficiency. In reality, it looks like the same old banking system just wearing a blockchain skin. If you are wondering what are tokenized stocks on coinbase, the answer is a digital receipt for a share held by a corporate entity, not a sovereign asset. We previously covered tokenizing the back office for more background.

What are tokenized stocks on coinbase?

To put it simply, tokenized stocks are digital representations of traditional shares that exist on a blockchain. Instead of a legacy brokerage holding your Apple or Tesla shares in a siloed database, a digital token represents that ownership. For the retail user, this means the ability to buy fractional shares of high priced stocks without needing a traditional broker info.arkm.com.

The vision is a world where any asset can be sliced into smaller units and traded instantly schwab.com. However, there is a massive gap between a tokenized asset and on-chain ownership. Most of these products are wrapped assets. The exchange holds the real stock in a vault and gives you a digital receipt. You aren't interacting with a decentralized ledger to prove ownership; you are trusting Coinbase or BlackRock to tell you that you own a piece of a company.

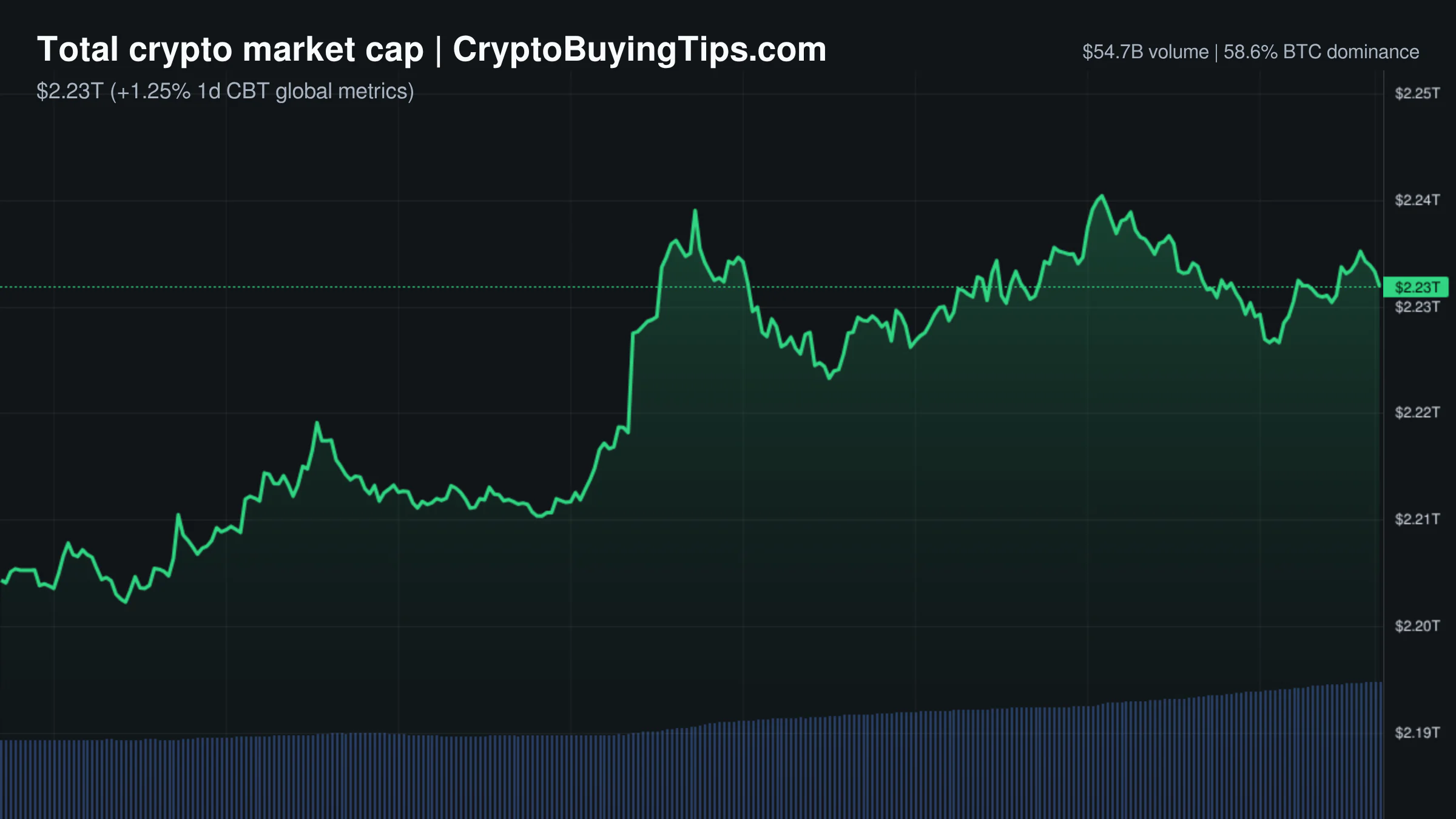

This is a far cry from the original promise of crypto. We are moving toward a total market cap of $2.51T, but if the most innovative use of that capital is just putting a ticker symbol inside a token, we aren't actually decentralizing anything.

Why institutional interest might be misreading on-chain activity

The narrative is that institutional giants like BlackRock are bringing the world on-chain. Our news scoring system identified BlackRock's BITA as a high-impact event, and the market usually reacts to these announcements with a wave of optimism. But the data on the ground tells a different story.

If the world's largest asset managers were actually migrating massive amounts of equity and debt onto the Ethereum network, we would see it in the gas fees. Instead, the current ETH gas fee is sitting at a negligible 0.14 Gwei. That is a level of network inactivity that suggests almost no one is actually using the chain for high-frequency institutional settlement.

The institutional adoption we are seeing is largely happening in the wrapper. BlackRock and Coinbase are building the interfaces, but they are doing it in a way that keeps the control centralized. They aren't using the blockchain to remove the middleman; they are using the blockchain to become a more efficient middleman.

The difference between tokenized assets and core crypto demand

We need to separate the hype of the everything app from the actual metrics that drive network value. There is a tendency to conflate the growth of tokenized Real World Assets (RWA) with the growth of blockchain utility. They are not the same.

When a stock is tokenized on a centralized exchange, the blockchain part is often just a ledger for the exchange's internal accounting. It doesn't create the same demand for decentralized compute or liquidity that a native DeFi protocol does. Our news scoring system rated the current trend of tokenized funds 9/10 for novelty, but novelty does not equal network demand.

Look at the broader market structure. BTC dominance is at 58.42%, showing that capital is still huddling in the safest, most liquid asset during this period of Fear (Fear & Greed Index: 25). If tokenized stocks were a genuine catalyst for a new market regime, we would see a rotation into the infrastructure that supports them. Instead, we see a volume collapse and a network that is essentially idling.

The structural risk of the everything app

The danger here is the illusion of diversification. By moving stocks into a crypto-adjacent everything app, users are concentrating their counterparty risk. If your BTC, your ETH, and your tokenized S&P 500 shares all live under one corporate roof, you have successfully recreated the single point of failure that crypto was designed to solve.

We've seen this play out before. We previously covered how tokenized IPOs often leave investors betting on a price feed rather than owning an actual asset. The risk is that these digital equities can be censored, frozen, or confiscated by the intermediary with a single click cointelegraph.com.

The everything app trade is a trap because it trades the security of the legacy system and the sovereignty of the crypto system for a bit of convenience in a mobile app. It's a polished product that masks a deep structural vulnerability.

What we're watching next

We are ignoring the press releases and watching the gas. Until we see a sustained move away from 0.14 Gwei, the institutional tokenization narrative is just marketing. We are also tracking whether this centralization leads to a liquidity crunch in native DeFi as capital gets sucked into these walled gardens. If the everything app continues to grow while on-chain activity stays dead, we are looking at a future where blockchain is just a database for the big banks.

Some links in this article may be affiliate links. We may earn a commission at no extra cost to you — this never influences our analysis or coverage.

Sigrid Voss

Crypto analyst and writer covering market trends, trading strategies, and blockchain technology.

More Articles

The altcoin season index is lagging and our DEX data shows the rotation has already started

The altcoin season index reads neutral while our proprietary data shows significant spikes in high-beta assets on…

Crypto Market Overview | Leveraged volume spikes amid fear index divergence | July 27, 2026

Crypto market overview shows leveraged volume spiking despite fear index readings; learn what institutional flows mean…

Ethereum ETFs are buying the dip while the network goes silent

Ethereum ETF flows show steady institutional buying despite low on-chain activity; our read is that right now, money…

Crypto Market Overview | Volume collapse masks marginal gains amid regulatory noise | July 26, 2026

Volume collapse masks marginal gains amid regulatory noise Crypto market overview for July 26, 2026 data points.